From a case of manipulating the securities market on the New Third Board, do the deduction standards for illegal gains and lending accounts constitute accomplices?

The New Third Board, also known as the National Equities Exchange and Quotations (NEEQ), has different market positioning, trading mechanisms, and liquidity levels from the Shanghai and Shenzhen Stock Exchanges. It adopts market making and agreement transfer methods in trading. The New Third Board has the characteristics of inactive trading, discontinuous trading prices, and significant fluctuations. Despite the continuous increase in the number of securities crimes, there are few precedents related to securities crimes on the New Third Board. In June 2017, the first case of illegal operation of New Third Board stocks in China was judged by the People's Court of Jing'an District, Shanghai. Hong and others were sentenced to imprisonment ranging from nine months to three years for the crime of illegal operation. The defendants did not appeal and the judgment has come into effect. After the first case, in September 2021, the Intermediate People's Court of Yichun City, Jiangxi Province, made a first instance judgment against Zhou and eight others. As one of the few public cases related to the New Third Board, this case is worth exploring the two controversial issues of "whether commission payments can be deducted" and "the threshold for criminalizing lending accounts". It has reference significance for the legal application of similar cases in the future. Based on these two issues, the author has compiled the following precedents for readers' reference.

1、 Case Introduction

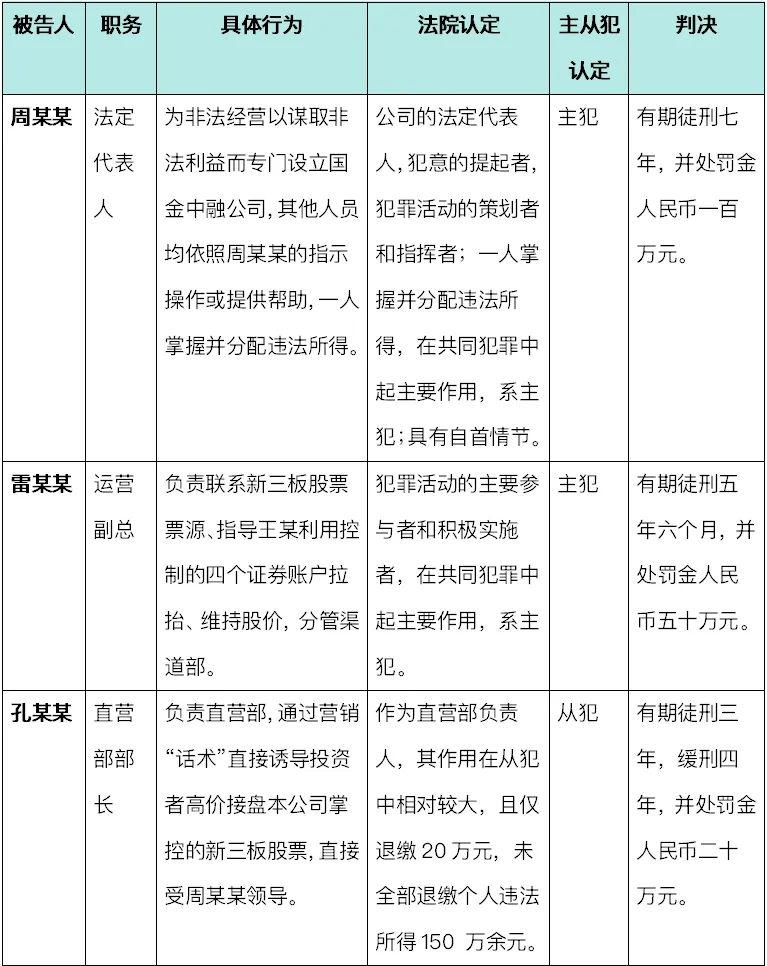

Since 2016, the defendant Zhou has established and controlled Guojin Zhongrong Company, planning to seek illegal benefits by manipulating the National Equities Exchange and Quotations (NEEQ) system for small and medium-sized enterprises. The company has established a "channel department" and a "direct sales department", which fabricate false and significant insider information about the stocks involved, such as the imminent IPO review and the short-term conversion to the A-share market. They use packaging personnel and maintain long-term contact with investors to gain trust, induce investors to take high positions, and earn high profit margins. The prosecution believes that Zhou, together with seven other defendants, used four securities accounts under his actual control to manipulate the trading prices and volumes of eight New Third Board stocks, including "Hunan Bamboo", through methods such as agreed trading, self buying and self selling, and manipulative trading. They illegally profited 141 million yuan, with a particularly large amount of illegal gains. In the end, the court sentenced all eight of them to the crime of illegal business operations.

2、 Controversy Focus 1: Can the rebate amount be deducted from illegal gains?

Zhou and others purchased a large number of New Third Board stocks to establish positions through the following two methods: one is to directly purchase stocks from original shareholders or agents at a low price; One method is to collude with the original shareholders or agents to agree on a low price in advance, but purchase stocks at a high market price. After completing the transaction, the original shareholders or agents privately refund Zhou, thus still achieving the actual purchase of stocks at a low price while keeping the market price high, inducing investors to make investment decisions. Out of the illegal profits of 141 million yuan, a total of 129 million yuan was returned to the agent as commission. The defense believes that the profit amount should be deducted from the amount of the commission to the distributor as agreed in the intermediary contract, and that the commission is the consideration of the legal intermediary contract and should be deducted from the illegal gains, with only the net income being held accountable.

The court holds that:

The rebate amount should not be deducted from illegal gains. The reason is that Zhou et al. manipulated eight New Third Board stocks they held through agreed trading manipulation and wash selling manipulation, and then sold the stocks through agents or direct manipulation to obtain illegal benefits. The act of agents selling stocks is part of Zhou et al.'s illegal operation, and the rebates obtained by agents are Zhou's distribution of illegal benefits. It is determined that the illegal gains of Zhou et al. from manipulating securities cannot be deducted from the amount refunded to the agent, and the actual amount obtained will be considered as a discretionary sentencing circumstance.

Related regulations:

According to Article 9 of the Interpretation on Several Issues Concerning the Application of Law in Handling Criminal Cases of Manipulating Securities and Futures Markets (Interpretation [2019] No. 9, hereinafter referred to as the "Interpretation") issued by the Supreme People's Court and the Supreme People's Procuratorate, "illegal gains" from manipulating securities refer to the benefits obtained or losses avoided through manipulating securities and futures markets. From this article, it can be seen that illegal gains in the legal sense are not equivalent to the actual amount obtained. Illegal gains emphasize the causal relationship between manipulative behavior and profit/loss avoidance. Only the benefits obtained or losses avoided through manipulative behavior can be recognized as illegal gains. In administrative law enforcement and judicial practice, the calculation of illegal gains usually starts from the occurrence of manipulative behavior and ends at the termination of manipulative behavior, elimination of manipulative influence, termination of administrative investigation, or other appropriate starting points. [1] Although commission rebate behavior has formal contracts, it occurs in an illegal manipulation system and is essentially a redistribution of illegal gains, without the attribute of "legal transaction costs".

The case of Li et al.'s manipulation of securities in the People's Court Case Library (2024-04-124-001) points out that illegal gains should first be recognized for profits such as trading spreads and residual bond values during the manipulation period, and then normal trading costs should be removed from them. Profits generated by other market factors should not be deducted in principle, and illegal costs such as allocation interest and account rental fees are not necessary expenses generated by normal trading activities and should not be deducted. Illegal gains shall be calculated based on the standard of profit amount, which is the total income from manipulating securities trading after deducting costs such as the amount of securities purchased and transaction taxes. The calculation formula for illegal gains is: illegal gains=total income from manipulating securities trading - purchase amount of securities - transaction taxes - other costs. Profits generated by other market factors should not be deducted in principle, and illegal costs such as allocation interest and account rental fees are not necessary expenses generated by normal trading activities and should not be deducted. ”[2]

What situations can be deducted from illegal gains?

According to the court's ruling, normal transaction costs can be deducted from illegal gains. According to Article 51 of the Guidelines for Determining Securities Market Manipulation (Trial) (now abolished), when calculating the amount of illegal gains, the following formula or other formula recognized by the expert committee can be referred to: illegal gains=market value of securities held on the end date+cumulative selling amount+cumulative cash out amount - cumulative buying amount - rights issue amount - transaction costs. Among them, transaction fees refer to taxes and fees already paid to the state, transaction commissions paid to securities companies, registration and transfer fees, and other reasonable transaction fees during the transaction.

Although the Guidelines for the Identification of Securities Market Manipulation (Trial) have been abolished, they are still an important reference for identifying illegal gains from securities market manipulation crimes in practice. The expenses that should be deducted listed in the "Guidelines for Determining Securities Market Manipulation (Trial)" are all direct costs of the perpetrator manipulating the market, while indirect costs such as wages, bonuses, venue leasing, and equipment purchases for the purpose of implementing manipulation are related to manipulation and are often seen as "manifestations of abuse of advantageous resources" in practice. Therefore, they are part of the criminal act itself and are not included in the deduction scope.

3、 Controversy Focus 2: Does lending an account alone constitute an accomplice?

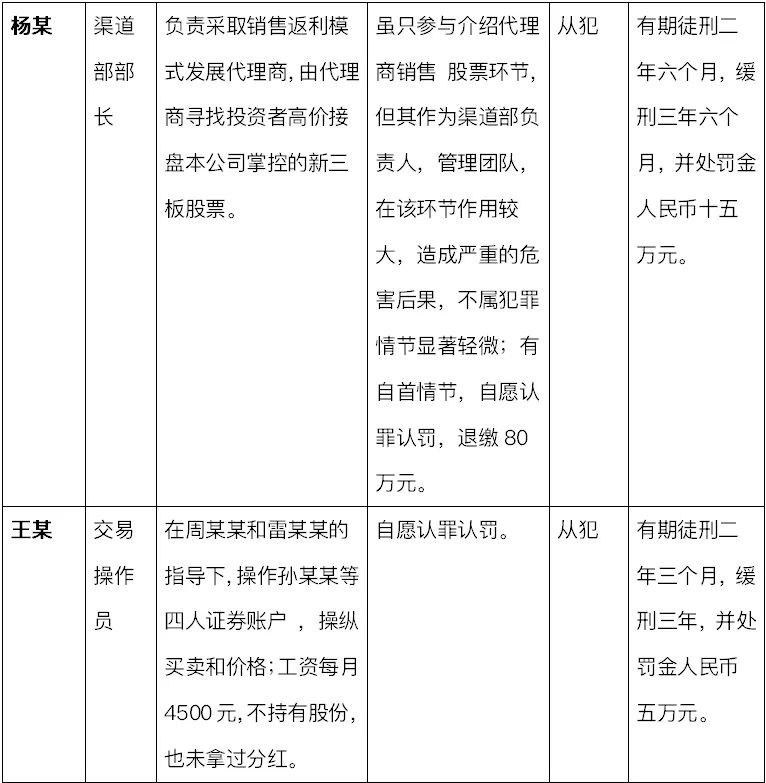

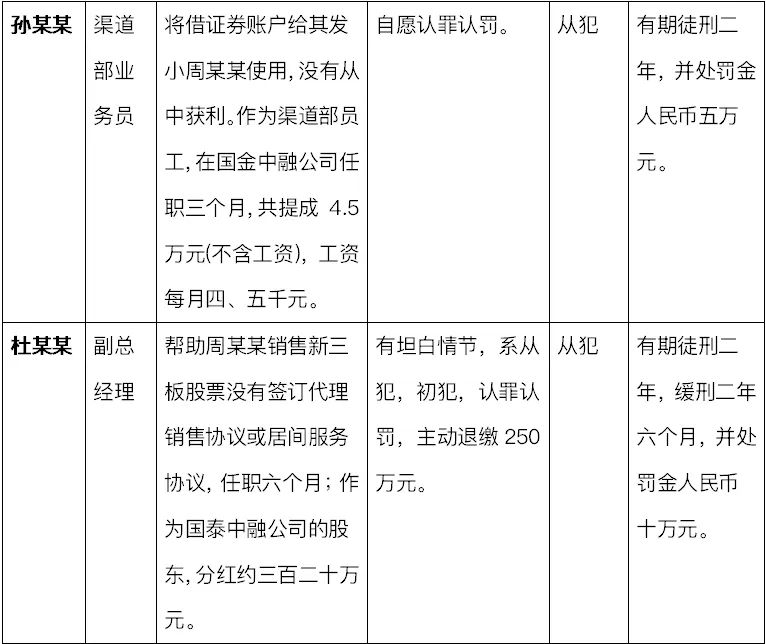

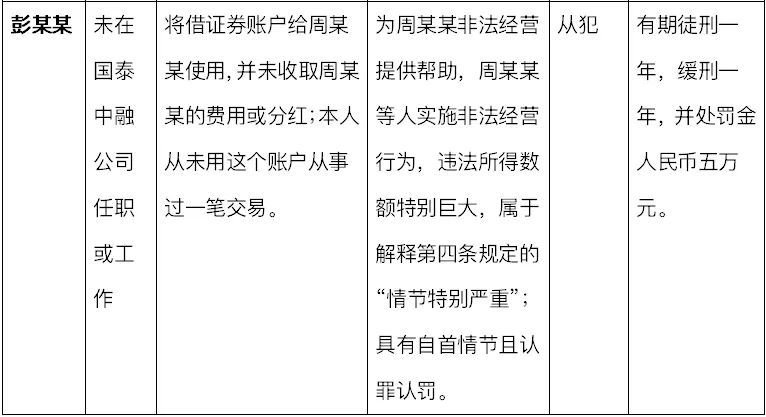

In this case, at the request of Zhou, Du, Sun, and Peng handed over their own New Third Board securities accounts to Zhou and formed a securities account group with Zhou's securities account, which was uniformly controlled by Zhou. Among them, Sun argued that he and Zhou had a childhood relationship and lent their accounts purely to help, without making any profit from it; Peng also argued that he only lent the account and did not make any profit or receive any dividends.

The court held that the three individuals, knowing that Zhou had collected securities accounts from them for illegal business operations, were still instructed by Zhou to provide securities accounts to Zhou. This behavior still constitutes the crime of illegal business operations. The basis for the court's determination that the three individuals were "aware" has the following commonalities, in my opinion:

Firstly, all three individuals have connections with the company. Peng's husband Zhao Gang is in a partnership with Zhou and has knowledge of all of Zhou's operations. Additionally, Peng's father Yan has been packaged by Zhou as a retired soldier and company executive; Du is a shareholder of the company; Sun is an employee of the company's channel department.

Secondly, all three have received warning letters more than once. For the first time, the stock transfer system discovered that there was reverse trading behavior in the securities accounts of Zhou, Sun, Du, and Peng during the trading of "Hunan Bamboo" stocks. On June 16 and July 24, 2017, they respectively issued decisions requiring the above-mentioned individuals to submit written commitments to self regulatory measures. Later, all four individuals submitted compliance trading commitment letters; For the second time, the stock transfer system discovered that Sun's account had repeatedly declared and traded "Weilong Zaizao" stocks at the boundary price of the declared effective price range, seriously affecting the closing price of the stock. On October 18, 2017, a decision was issued to Sun again to submit a written commitment to self regulatory measures. Sun submitted a compliance commitment letter on October 20, 2017. For the third time, the stock transfer company discovered that from January 15 to March 28, 2018, four securities accounts had repeatedly deviated significantly from the latest transaction price revealed by the stock market during the trading process of the innovative layer's call auction stock "Kaixin Shares", and had traded with fixed accounts, seriously affecting the closing price of the stock and constituting a violation of stock trading regulations. On April 9, 2018, the company decided to take self regulatory measures by issuing warning letters to Zhou and four others.

That is to say, the court will only convict the perpetrator if there is evidence to prove that the perpetrator subjectively "knew" that others were collecting accounts from them for the purpose of committing a crime, otherwise criminal responsibility should not be pursued. Based on the circumstances of the three individuals mentioned above and other sentencing circumstances, the court makes the following judgment:

Specific behaviors and differences of master-slave offenders

Regarding the criteria for determining master-slave offenses, although the actions carried out by the same criminal gang as a whole can be classified as market manipulation, at a micro level, the actions carried out by the perpetrator are usually a part of market manipulation. At this point, the principal and accomplice should be determined based on the substantive role of the perpetrator in the joint crime. If the perpetrator plays a major role in participating in and actively carrying out the crime, they are the principal offender and should be punished according to all the crimes they have participated in. If the perpetrator mainly accepts instructions and plays a secondary role in the crime, they are considered accomplices and should be given a lighter punishment according to law.

In this case, Zhou is the legal representative of the company, the initiator of the criminal intent, the planner and commander of the criminal activity, and other personnel operate or provide assistance according to Zhou's instructions. The illegal gains are controlled by Zhou alone and distributed by him. He plays a major role in the joint crime and is the principal offender. Although Sun, Du, and Peng did not directly operate the account, they knowingly provided it to manipulate transactions, demonstrating subjective knowledge and objective cooperation. They played a secondary role in the crime and constituted accomplices.

4、 Three insights

1. The determination of illegal gains emphasizes functional logic over formal contracts: even if there is a nominal contractual arrangement, as long as it is a part of the illegal transaction chain, it does not constitute a deduction item.

2. The "peripheral participants" involved in manipulative behavior also need to bear responsibility: seemingly "marginalized" behaviors such as lending securities accounts and cooperating with false advertising may be recognized as accomplices in judicial practice.

3. The New Third Board is not equivalent to a "regulatory exemption zone": This case has clearly cracked down on manipulative behavior in the New Third Board market, sending a clear signal that the judicial system has "zero tolerance" for such behavior.

Attachment: Overall verdict of the eight defendants in this case:

Related recommendations

- From a case of manipulating the securities market on the New Third Board, do the deduction standards for illegal gains and lending accounts constitute accomplices?

- The latest arbitration award resonates with the Judicial Interpretation on Labor Disputes (II) on the same frequency - the exception of double wages without signing a written contract

- How to bear the legal responsibility for lost and damaged packages in drone express delivery

- The Legal Validity and Qualitative Analysis of Game Training Contracts